Note Provisions for pensions and similar obligations

Defined benefit plans

The Group maintains defined benefit retirement plans in

which employees earn the right to payment of benefits after

completing their employment, based on their final salary and

period of service. These defined benefit retirement plans exist

in Sweden, the Netherlands, Belgium, and India. There are

further commitments for retirement and survivors’ pensions

for salaried employees in Sweden that are insured through

Folksam (Folksam cooperative occupational pensions).

The obligations for retirement and survivors’ pension for

salaried employees in Sweden are insured through policies

with Alecta or correspondingly in Folksam. According to a

statement by the Swedish Financial Reporting Board, UFR 3,

classification of ITP plans financed via insurance with Alecta,

this is a defined benefit plan that involves several different

employers. For the period from January 1 to December 31,

2019, AAK AB and AAK Sweden AB have not had access to

sufficient information to recognize their proportional shares

of the plan’s obligations, plan assets and costs, which has

meant that it has not been possible to recognize the plan as

a defined benefit plan. The ITP 2 pension plan that is insured

through Folksam is therefore recognized as a defined contribution

plan. The premium for the defined benefit retirement

and survivors’ pension is calculated individually and depends

on factors including salary, pension earned previously and

expected remaining period of service. Charges for ITP 2

pensions insured through Folksam are SEK 17 million (14).

The collective consolidation level consists of the market

value of Alecta’s assets as a percentage of the estimated

insurance commitments, computed using Alecta’s actuarial

methods and assumptions, which are not in accordance with

IAS 19. The collective consolidation level should normally be

permitted to vary between 125 and 155 percent. If Alecta’s

collective consolidation level is below 125 percent or above

155 percent, measures must be taken to create the conditions

for the consolidation level to return to the normal range. If

the consolidation is low, one measure may be to increase

the agreed price for new policies and increasing existing

benefits. If the consolidation is high, one measure may be to

introduce premium reductions. At year-end 2019, Alecta’s and

9

Folksam’s surplus in the form of their collective consolidation

levels was 148 percent and 187 percent, respectively (142

percent and 174 percent, respectively).

The Group has defined benefit pension plans in Sweden

and the Netherlands which come under largely similar

regulations. All plans are pension plans based on final salary

and give employees covered by the plans benefits in the form

of a guaranteed level of pension payments during their lives.

The level of the benefits depends on the employees’ period

of service and salary on retirement. The pension payments in

the Swedish and Dutch plans are normally indexed according

to the consumer price index. The plans are subject to largely

similar risks. Benefits are paid from plans that are secured

with foundations. The activities of the foundations are regulated

by national regulations and practice which also apply

to the relationship between the Group and the administrator

(or equivalent) of the foundation’s plan assets. Responsibility

for monitoring the plans, including investment decisions and

contributions, is held jointly by the company and the foundation’s

board.

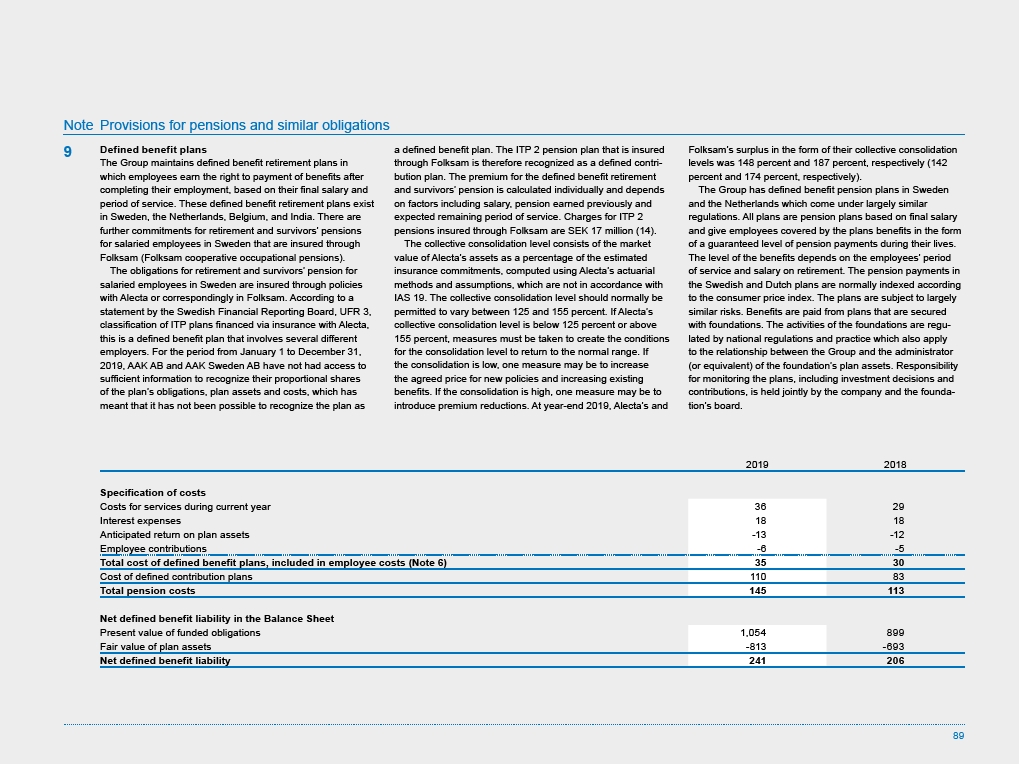

2019 2018

Specification of costs

Costs for services during current year 36 29

Interest expenses 18 18

Anticipated return on plan assets -13 -12

Employee contributions -6 -5

Total cost of defined benefit plans, included in employee costs (Note 6) 35 30

Cost of defined contribution plans 110 83

Total pension costs 145 113

Net defined benefit liability in the Balance Sheet

Present value of funded obligations 1,054 899

Fair value of plan assets -813 -693

Net defined benefit liability 241 206

89